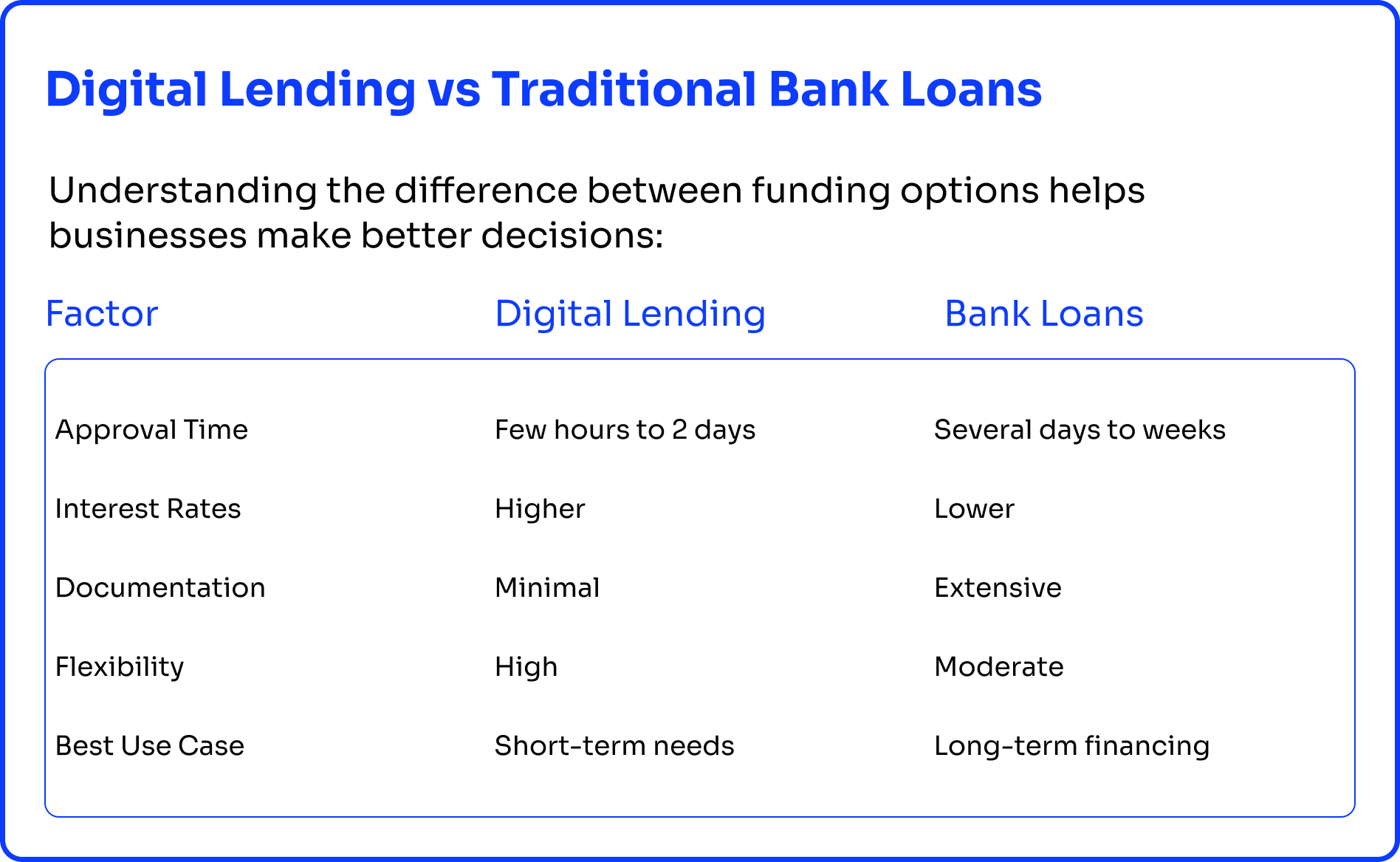

When founders first turn to digital lending platforms, the appeal is obvious. Approvals are fast, documentation is minimal, and funds can arrive within hours. For SMEs and MSMEs, this feels like a lifesaver, especially when cash is tight.

Initially, everything works well. A short-term loan covers payroll, another supports urgent inventory needs, and the business manages small liquidity gaps with ease.

But over time, a subtle problem begins to surface. Multiple short-term loans begin to accumulate. Interest costs increase quietly. Repayments begin to overlap, creating confusion and making visibility into total borrowing unclear.

The issue is not digital lending itself. The real problem lies in how businesses use it.

Where Most SMBs and MSMEs Go Wrong

Even though digital lending is fast and convenient, many businesses make decisions that increase costs and create financial stress. The most common gaps include:

- Using digital lending for everything

Many founders rely on digital loans for long-term projects, expansion, or the purchase of fixed assets. These loans are designed for short-term needs. Using them for long-term purposes significantly increases borrowing costs.

- Ignoring the blended cost of capital

Businesses often look at individual loan rates instead of the combined impact of multiple loans. When several loans run at the same time, the total interest burden becomes much higher than expected.

- Lack of visibility across borrowings

Loans taken from different platforms create a fragmented view of debt. Repayments overlap, obligations become unclear, and managing cash flow becomes difficult.

- Reactive borrowing

Many business owners borrow only when cash runs out. This limits planning and forces quick decisions, often leading to higher costs and reduced flexibility.

The Right Way to Use Digital Lending

Digital lending works best when used strategically. Businesses should use it for:

- Short-term working capital gaps

- Urgent business opportunities

- Invoice-based funding

- Seasonal demand spikes

These are situations where speed matters and traditional finance may be too slow.

At the same time, businesses should avoid using digital lending for long-term expansion, fixed asset purchases, or large structured financing. These needs are better served by banks or NBFCs, which offer lower costs and longer repayment cycles.

Understanding Interest Rates in Digital Lending

One of the most important factors to consider is cost. Digital lending platforms charge higher interest rates compared to traditional institutions due to speed and accessibility.

- Digital lenders: 18% to 36% annually

- NBFCs: 12% to 24% annually

- Banks: 8% to 14% annually

While digital lending offers convenience, the higher cost makes it suitable mainly for short-term use.

Popular Digital Lending Platforms in India

Several platforms provide quick and accessible business loans in India. Some commonly used ones include:

- Lendingkart

- PolicyBazaar

- Paytm

- Pine Labs

- MoneyTap

These platforms offer fast approvals and minimal documentation, making them useful for immediate funding needs.

The Ideal Financing Mix

A well-structured SMB or MSME uses a mix of funding sources. Banks provide low-cost long-term capital. NBFCs offer flexible mid-term funding. Digital lending adds speed for short-term needs. Digital lending should be treated as a liquidity buffer, not the primary source of funding. This approach helps maintain flexibility without increasing financial pressure or affecting the company’s financial situation.

The Real Enabler: Financial Visibility

The biggest mistake is not borrowing. It is borrowing without clarity. To use digital lending effectively, businesses need complete visibility into their finances. This includes:

Clear view of all bank balances

- Tracking inflows and outflows

- Awareness of repayment timelines

- Understanding total debt exposure

Without this, even fast access to credit can create confusion and stress.

How Yobo Helps

Many SMBs and MSMEs are now turning to platforms that provide real-time financial visibility. Tools like Yobo help businesses consolidate financial data, track liquidity, and monitor cash movement across accounts.

With better insights, businesses can plan to borrow decisions more effectively, avoid overlaps, reduce costs, and use digital lending as a strategic tool rather than a reactive solution.

Final Takeaway

Digital lending is one of the most powerful tools available to modern businesses. Its impact depends entirely on how it is used.

When used correctly, it improves agility, supports cash flow, enables growth, and plays a key role in reducing the risk of financial strain. When used without structure, it increases financial pressure and reduces clarity.

The difference lies in planning, visibility, and discipline. In today’s business environment, speed without clarity can become expensive.

FAQs

What is the typical interest rate for digital lending platforms?

Interest rates usually range from 18% to 36% annually, depending on the lender and risk profile.

Are digital lending platforms safe for businesses?

Yes, if businesses choose regulated and well-known platforms and review all terms carefully before borrowing.

How quickly can businesses receive funds through digital lending?

Most platforms disburse funds within a few hours to 48 hours after approval.

When should a business choose a bank loan instead of digital lending?

Bank loans are better for long-term needs because they offer lower interest rates and structured repayment options.