India’s digital payment ecosystem grew on one promise: speed. UPI made instant transfers feel effortless, cards became seamless at checkout, and mobile wallets turned everyday payments into a matter of seconds. For millions of users, fast payments stopped feeling innovative and simply became normal.

Now, RBI’s new two factor authentication rule is changing that experience across the ecosystem.

The system is not slowing down because the rails are weak. It is slowing down because digital payments have now reached a scale where speed alone is no longer enough. Fraud methods such as phishing, SIM swap attacks, and device level manipulation have exposed the weakness of relying on a single layer of confirmation.

This is why payments are now being redesigned around trust and intent, not just movement of money.

The real shift is simple: a payment is no longer complete just because funds moved successfully. It is complete only when the system can confirm that the right user actively approved it in that exact moment.

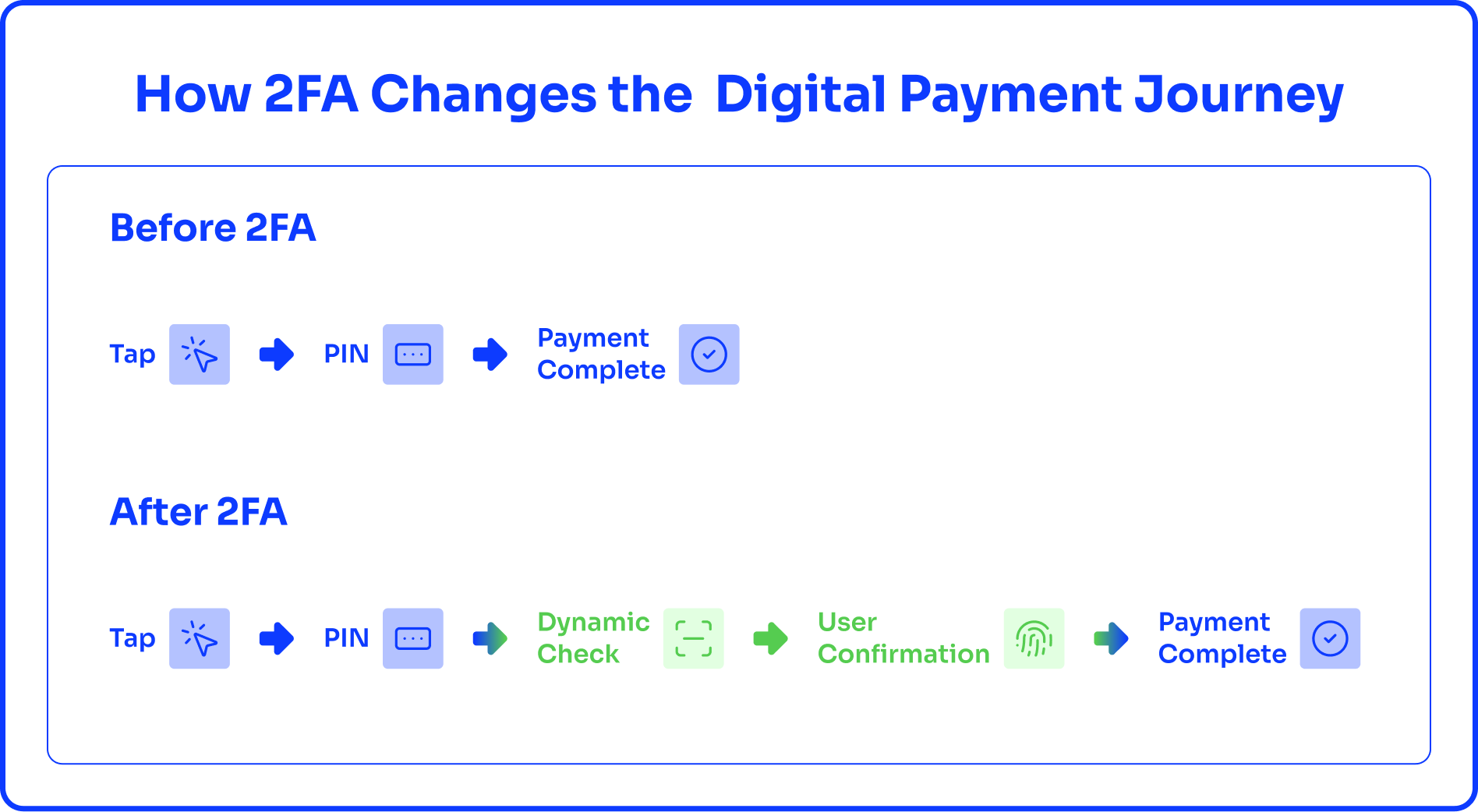

What Has Actually Changed in Digital Payments

Under RBI’s updated framework, every digital transaction now needs at least two separate authentication factors, with one factor dynamically linked to the specific transaction. This applies across UPI, online card payments, wallets, and digital banking experiences.

For everyday users, this means OTP alone may no longer be enough. A payment may now require an additional PIN, biometric confirmation, secure token, or trusted device validation depending on the app, bank, and transaction risk.

This may only add a few seconds to the checkout flow, but it changes how users experience digital payments.

The transaction journey now includes an extra moment of awareness, where users actively verify what they are paying, who they are paying, and whether the transaction was truly initiated by them.

How This Will Change the Consumer Payment Experience

For consumers, the biggest visible change will be now during checkout.

A UPI transfer that earlier needed only a PIN may now require an extra layer on some transactions. Card payments on shopping sites may ask for biometric confirmation or stronger app-based approval. Wallet payments could introduce device trust checks when the user logs in from a new phone.

In practical terms, the payment remains fast, but it may no longer feel invisible.

That matters because India’s digital payment growth was built on reducing friction. Now the ecosystem is adding smart friction, where low risk payments remain smooth while higher risk transactions trigger stronger verification.

This change may slightly affect impulse purchases and instant checkout behaviour, especially for users who are used to one tap of payment experiences.

What This Means for Merchants and Businesses

The merchant side impact is equally important.

Every extra verification layer can influence checkout completion rates, especially in ecommerce, subscriptions, and mobile first purchases. If users face additional confirmation steps, some may abandon transactions midway, while others may take longer to complete purchases.

At the same time, stronger authentication improves customer trust.

Users become more confident while paying on unfamiliar websites, higher ticket purchases, or first-time merchant checkouts because the system visibly reassures them that the payment is secure.

For businesses, this creates a tradeoff between slightly more friction and significantly better trust.

In the long term, better trust usually improves digital payment adoption more than raw speed alone.

The Bigger Impact on India’s Payment Ecosystem

The bigger change is at the ecosystem level. India’s digital payment infrastructure is moving from speed-first design to risk-aware design. Trusted devices, low-value payments, and familiar user behaviour may continue to stay fast, while suspicious devices, unusual payment patterns, or high-value transfers may trigger stronger checks.

This makes the ecosystem smarter. Instead of treating every transaction the same way, banks and payment apps now apply authentication based on transaction context.

That means the future of digital payments in India will likely become:

- faster for trusted behaviour

- stricter for risky behaviour

- safer for users overall

This is a major evolution in how payment systems scale securely.

The Real Reframe

Every major change in India’s payment journey first feels like friction. Then it becomes trust infrastructure. The same will happen here.

RBI’s new two factor authentication rule is not just adding one more step to UPI, cards, or wallets. It is redefining how trust gets built into every digital payment experience in India. The real question is no longer whether payments stay fast. It is whether they stay fast enough while becoming significantly safer.

FAQs

Will UPI payments become slower?

UPI payments will remain fast, but some transactions may now include an extra verification step based on risk and device trust.

Will this affect card and wallet payments too?

Yes, the rule applies across UPI, cards, wallets, and most domestic digital payment methods.

Will this reduce payment fraud?

Yes, the main purpose is to reduce phishing, SIM swap, and unauthorized transaction risks through stronger authentication.

Is this good for merchants?

Yes, while checkout may add slight friction, stronger trust can improve user confidence and long-term payment completion quality.