Effective cash flow management stands as one of the most demanding tasks for any business owner or financial director. While extra cash in the bank feels like a safety net, large sums in a standard current account often represent a missed opportunity. Inflation steadily erodes the purchasing power of your money, which means that idle cash effectively loses value every day it sits still.

For businesses looking for a balance between security and growth, Fixed Deposits (FDs) offer a reliable solution. This guide explores why businesses use FDs to protect their capital while earning a guaranteed return.

What is a Business Fixed Deposit?

A business fixed deposit is a financial product where a company invests a specific amount of money with a bank for a set period. In exchange for leaving the money untouched, the bank pays a higher interest rate than a standard current account. These terms can range from a few months to several years.

This type of account provides absolute certainty because while the stock market can fluctuate, your principal investment remains safe. You know exactly how much interest you will earn from the day you open the account.

Why Should Your Business Consider an FD?

Several distinct advantages exist for companies that choose to lock away their surplus funds for a set duration.

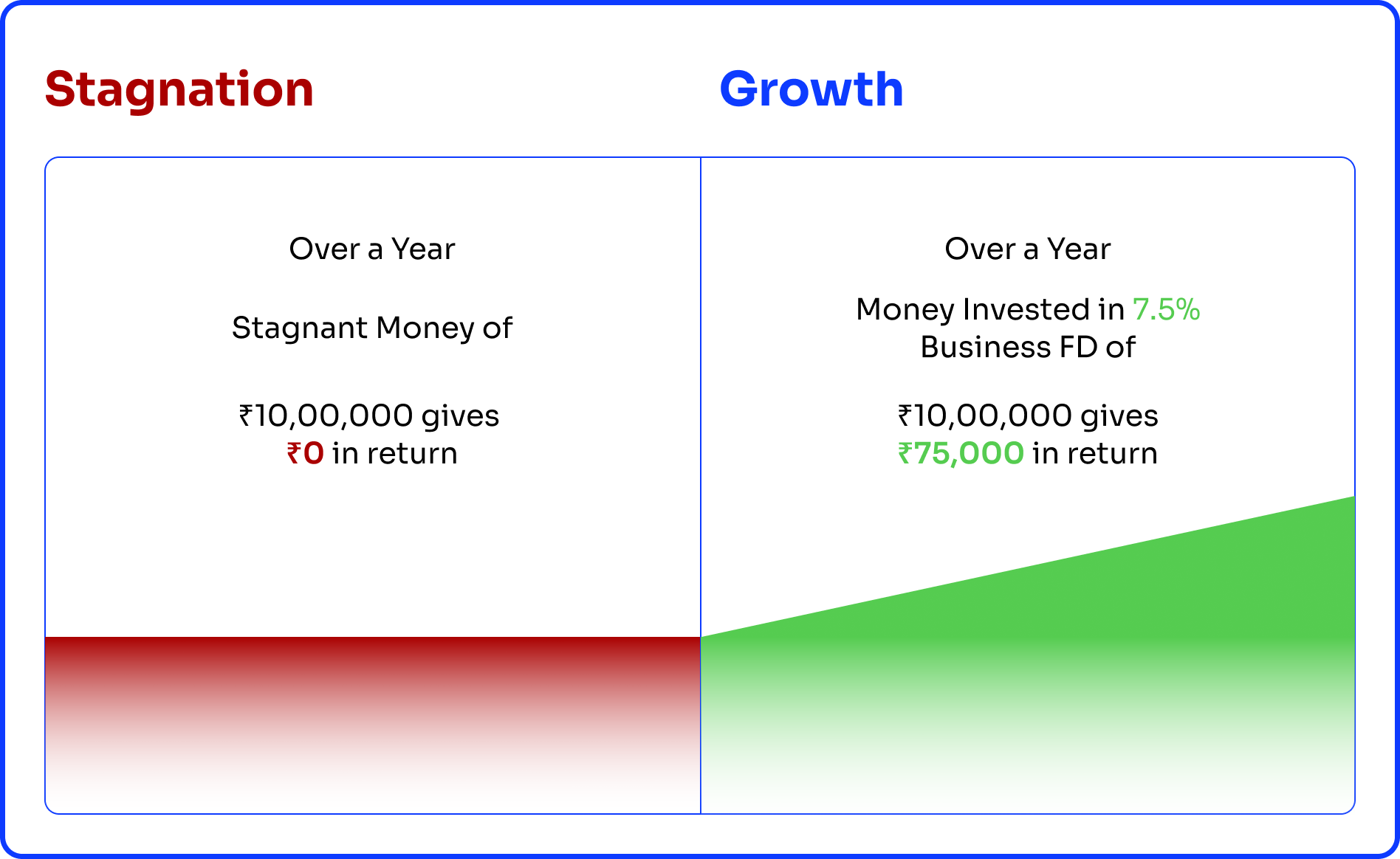

1. Capital Preservation: The primary goal for most businesses is safety. Whether you are saving for future tax bills, upcoming office expansions, or a rainy day fund, an FD ensures your initial investment is protected. In India, bank deposits are insured by the DICGC up to 5,00,000 INR (including principal and interest), making your money remarkably secure.

2. Guaranteed Returns: Market volatility can make other investment vehicles stressful for small and medium enterprises. With a fixed deposit, the interest rate is locked. Even if the RBI lowers repo rates during your term, your agreed rate remains the same. This allows for precise financial planning and forecasting.

3. Disciplined Saving: It is easy to dip into a current account for non essential expenses. By placing idle cash into an FD, you create a healthy barrier. The knowledge that early withdrawal usually carries a penalty encourages better financial discipline and ensures the money is available when the business truly needs it.

Solving the Problem of Idle Cash

The main problem this blog addresses is the concept of "lazy money." Many business owners are too busy with daily operations to manage a complex investment portfolio. Consequently, cash sits in accounts that pay zero or negligible interest.

Move that money into an FD to turn a static asset into an active one. It solves the dilemma of wanting to grow your money without taking on the risks associated with equity markets or property.

Key Factors to Consider Before Investing

You must evaluate a few essential factors to ensure the product matches your specific business needs before you commit your funds.

1. The Investment Term: Review your cash flow forecast for the next year. If you won't need certain funds for twelve months, a one year fixed term is ideal. However, for shorter term needs, look for 91 day or 180 day buckets which offer a middle ground between flexibility and high interest.

2. Interest Payment Frequency: Some banks pay interest monthly, while others pay it at the end of the term (cumulative). If your business requires a regular boost to its monthly cash flow, a monthly payout might be preferable. If you want to maximise the "compound" effect, a cumulative FD is better.

3. Minimum and Maximum Limits: Business FDs often have higher entry requirements than personal ones. Most banks require a minimum deposit of 1,00,000 INR for corporate accounts. Ensure your idle cash meets these requirements without stretching your operational liquidity too thin.

How to Get Started

Setup for a business FD is usually a straightforward process if you follow a few logical steps.

- Review your accounts: Identify the core balance that never leaves your account.

- Compare rates: Use a comparison tool to find the best business deposit rates currently available in India.

- Check the fine print: Look for any specific rules regarding early closure or "non-callable" deposits.

- Apply: Most applications are now digital and can be completed in minutes through your corporate net banking portal.

Final Thoughts

Fixed Deposits are not the most glamorous financial tool, but they are one of the most effective for sensible business management. They provide a sanctuary for your hard-earned profit, shielding it from market swings while allowing it to grow.

Placement of your idle cash into a fixed deposit ensures that every rupee in your business is working just as hard as you are. It is a simple, safe, and professional way to strengthen your balance sheet and prepare for the future.