Key Takeaways

· Cash flow forecasting business owner's plan.

· Regular forecasting improves control over expenses and payments.

· Simple forecasts support better financial decisions.

What is Cash Flow Forecasting and Why does it matter for SMBs & MSMEs?

Let’s understand it with an example

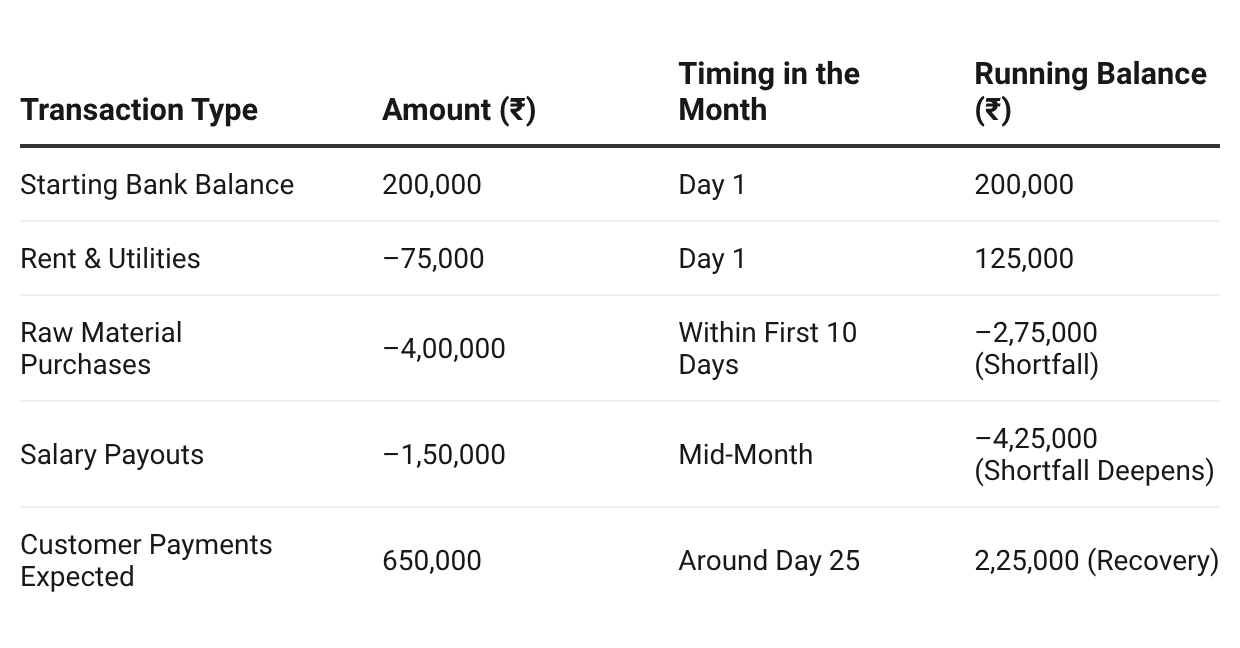

Ankur runs a small packaging business. While he receives payments from customers only after delivery, he is required to pay suppliers and employees on fixed dates. The table below presents his monthly cash flow forecast to help assess his liquidity position.

Even though the total money expected to come in during the month (₹8,50,000) is higher than the total expenses, the running balance clearly shows a mid-month liquidity gap of ₹4,25,000. This means the business may still face a temporary cash shortfall despite being profitable on paper.

So why does this temporary cash shortfall happen?

The answer lies in timing. Most expenses occur early in the month. Suppliers, rent, and salaries must be paid on fixed dates. However, customer payments typically arrive later usually after 20–25 days. This mismatch between when cash goes out and when it comes in creates pressure, even when total inflows eventually exceed total outflows.

Where did Ankur Go Wrong

Ankur’s issue wasn’t revenue. It was visibility and sequencing and that’s where most small businesses struggle with cash flow forecasting.

- Looking at totals instead of timing: — ₹6,50,000 in expected payments looked reassuring. But most of it was arriving after Day 25, while major expenses were due earlier. Many SMBs compare monthly inflows and outflows without mapping when cash actually moves.

- Not identifying the lowest cash point: — Ankur didn’t track his weekly running balance. If he had, the ₹4,25,000 shortfall would have been visible in advance. The lowest liquidity points matter more than the month-end balance.

- Treating receivables as guaranteed cash: — “Expected” payments are not received payments. Forecasting based on invoice due dates rather than actual collection behavior leads to overly optimistic planning.

- Accepting expense timing passively: — ₹4,00,000 in supplier payments were due within 10 days. Were those terms aligned with customer payment cycles? Many MSMEs accept outflow timing while hoping inflows arrive on schedule.

- Operating without consolidated visibility: — Whether one account or many, decisions made without a forward-looking, consolidated view will create blind spots. Most cash flow stress isn’t a revenue problem it’s a visibility problem.

To understand how to manage multi-bank accounts for a consolidate view Read

What Ankur Should Have Done Instead

He didn’t need more revenue. He needed visibility and sequencing

- Build a 13-Week Rolling Cash Flow Forecast: — A weekly 13-week rolling forecast would have revealed the ₹4,25,000 gap early.

The key question shifts from:

“Will the month end be positive?”

to

“Where is my lowest cash point?” - Separate Fixed and Flexible Outflows: — Salaries, rent, and statutory dues are fixed. Inventory and marketing often have flexibility.

Clear categorization allows staggered or deferred payments during tight weeks. - Forecast Based on Real Collection Patterns: — Receivables should reflect actual payment behavior, not invoice due dates.

Probability-adjusted forecasting dramatically improves working capital planning. - Use an AI-Native Tool and Maintain a Liquidity Buffer: — An AI-native platform that consolidates bank accounts and generates forward-looking projections improves visibility and reduces manual errors.

And every SMB & MSME should maintain a liquidity buffer covering at least one payroll cycle and essential vendor payments.

Final Takeaway

Ankur’s challenge was timing, visibility and not revenue.

When inflows, outflows, and lowest cash points are clearly mapped, decisions become calmer and smarter.

For SMBs and MSMEs, disciplined cash flow forecasting:

- Strengthens working capital management

- Improves financial planning

- Reduces avoidable stress

To try auto-generating Cash Flow Analysis use Yobo.money

Bonus Insight

Jeff Bezos has once said that free cash flow is Amazon’s most important financial metric. Profits may look strong on paper, but real resilience comes from cash generation.

For small businesses, the lesson is simple:

Tracking sales isn’t enough. Planning cash flow is what protects survival.