When most businesses think about digital payments in India, they often assume there is a clear winner. Either UPI is taking over, or credit cards are driving higher value spending. The reality in 2026 is far more balanced. Indian consumers are not choosing one over the other. They are using both, depending on how much they spend and what they need in that moment.

This shift has important implications, especially for businesses that rely on digital checkouts. Payment preference is no longer a single choice. It is closely tied to transaction size and financial behavior.

A changing payment landscape

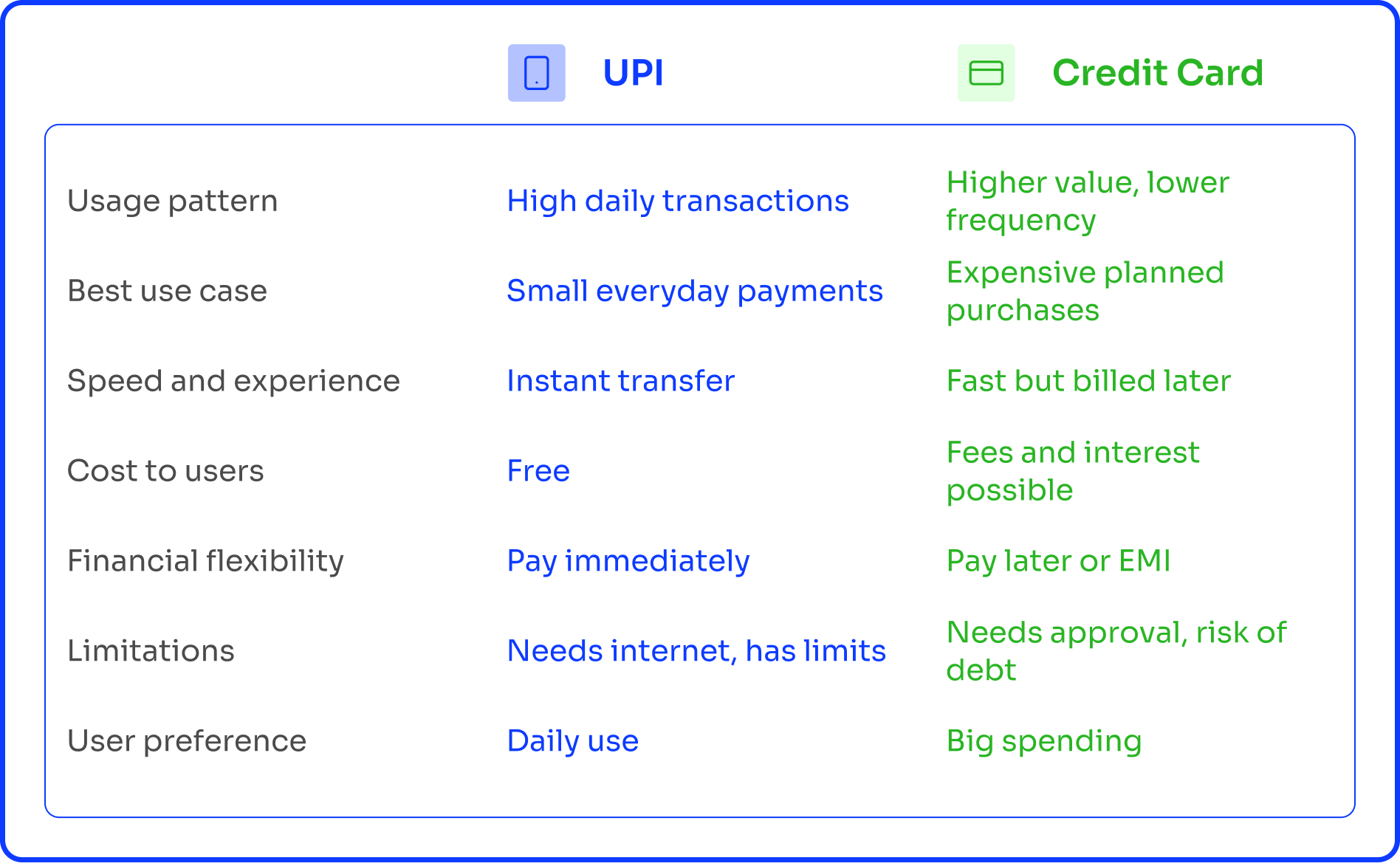

India’s move towards digital payments has reached a point where convenience is expected rather than appreciated. UPI has become the most widely used payment method in the country. It supports billions of transactions each month and works across all types of merchants, from small vendors to large platforms. Its strength lies in its simplicity. A quick scan or a mobile number is often all it takes to complete a payment.

At the same time, credit cards continue to grow in value even if their user base is smaller. They are especially popular among urban consumers who make planned purchases and value flexibility. Large transactions such as electronics, travel, and subscriptions often rely on credit cards because they allow users to manage cash flow more effectively.

This means both systems are growing at the same time, but in different ways. UPI dominates in volume, while credit cards dominate in value.

How spending size shapes payment choice

The clearest difference between UPI and credit cards appears when you look at transaction size.

For smaller purchases under ₹2,000, UPI is the natural choice. It is fast, simple, and requires no additional steps. Customers use it for everyday needs such as food, transport, and local services. In this range, ease matters more than flexibility.

For higher value purchases above ₹10,000, behavior changes. Customers start thinking about how the payment affects their finances. A credit card offers time to repay and often provides EMI options. These features reduce the immediate financial burden. If a business only offers UPI for such transactions, it may unintentionally create friction and lose potential buyers.

The middle range between ₹2,000 and ₹10,000 is less predictable. Both UPI and credit cards are used here, and the preference depends on the customer’s profile and intent. This is also where many businesses lack clear visibility into what their customers actually prefer.

A quick comparison of UPI and credit cards

What this means for businesses

For businesses, the key challenge is not choosing between UPI and credit cards. It is understanding how both function within their own checkout experience.

Many businesses rely on default payment gateway settings, which often priorities UPI. While this makes sense for volume, it may not support customers who want flexibility for larger purchases. The result is a gap that is not always visible. Customers who do not find suitable payment options often leave without completing the transaction.

There are two common gaps. One is the absence of EMI options for higher value transactions. Customers who need flexibility may hesitate to pay the full amount upfront. The other is inefficiency in recurring payments, where modern options could improve success rates but are not fully implemented.

These gaps do not always show up clearly in reports, which makes them easy to overlook.

Why visibility matters more than assumptions

Understanding payment behavior requires clear data. Businesses need to know how different payment methods perform across transaction values. They also need to identify where customers drop off and why.

This is where Yobo becomes relevant. Yobo brings together transaction data from multiple payment sources into a single view. It allows businesses to see how customers actually pay, rather than relying on assumptions.

With this clarity, it becomes easier to identify patterns. For example, a business may discover that higher value customers prefer credit cards, while smaller transactions rely heavily on UPI. It may also reveal where customers abandon transactions due to missing options.

Instead of making broad changes, businesses can make targeted improvements that directly affect conversions.

Final thoughts

In 2026, the conversation is no longer about whether UPI or credit cards are better. Both play important roles in India’s payment ecosystem. UPI leads in accessibility and frequency, while credit cards offer flexibility and value for larger transactions.

For consumers, the choice depends on the situation. For businesses, the priority should be to support both behaviors’ effectively. The more clearly you understand how your customers pay, the better you can align your checkout to meet their expectations.

FAQs

1. Do younger users prefer UPI over credit cards

Younger users often start with UPI because it is simple and accessible, but many adopt credit cards later for larger purchases and financial planning.

2. Can payment options influence customer trust

Yes, offering familiar and flexible payment options can improve trust and make customers more confident in completing a purchase.

3. Is it necessary to review payment performance regularly

Yes, customer behavior changes over time, so regular reviews help ensure that your payment setup remains effective.

4. How can businesses improve payment success rates

They can improve success rates by offering relevant payment options, simplifying checkout steps, and using data to identify and fix drop off points.