A small manufacturing business receives a large order but needs funds to buy raw materials. The founder approaches a bank, but the approval process may take several weeks. At the same time, a Non-Banking Financial Company (NBFC) offers faster funding at a higher interest rate.

The founder now faces a simple question. Should the business wait for the bank loan or choose the faster NBFC option?

Many businesses face this situation. Understanding how banks and NBFCs work helps founders make better financing decisions.

How banks evaluate businesses

To understand the financial health of a business, banks closely review a few key indicators.

Transaction Behaviour

Banks analyse the movement of money through the company’s bank accounts. Regular customer payments and consistent supplier transactions indicate stable business activity.

Business turnover and cash flow

Working capital limits often depend on the scale of the business. Banks review revenue patterns, operating costs, receivable cycles, and inventory requirements to estimate how much funding the business can manage responsibly.

Existing loans and repayment history

Banks also review current borrowing and repayment records. They want to ensure that additional credit will not create financial pressure on the company.

Credit score and CIBIL history

Banks and NBFCs also review the credit history of the business and its founders. In India, lenders commonly refer to the CIBIL score, which reflects the repayment behaviour of past loans and credit facilities.

A higher credit score signals financial discipline and increases the chances of loan approval. A lower score may lead to stricter conditions, smaller loan amounts, or even rejection.

For most lenders, a score above 700 is generally considered strong when evaluating business loan applications.

Collateral and security

Many bank loans require security such as property, inventory, or receivables. This protects the bank in case repayment difficulties arise.

Because banks follow structured and cautious processes, their loan approvals may take time. However, the interest rates are usually lower compared with other lenders.

How NBFCs evaluate businesses

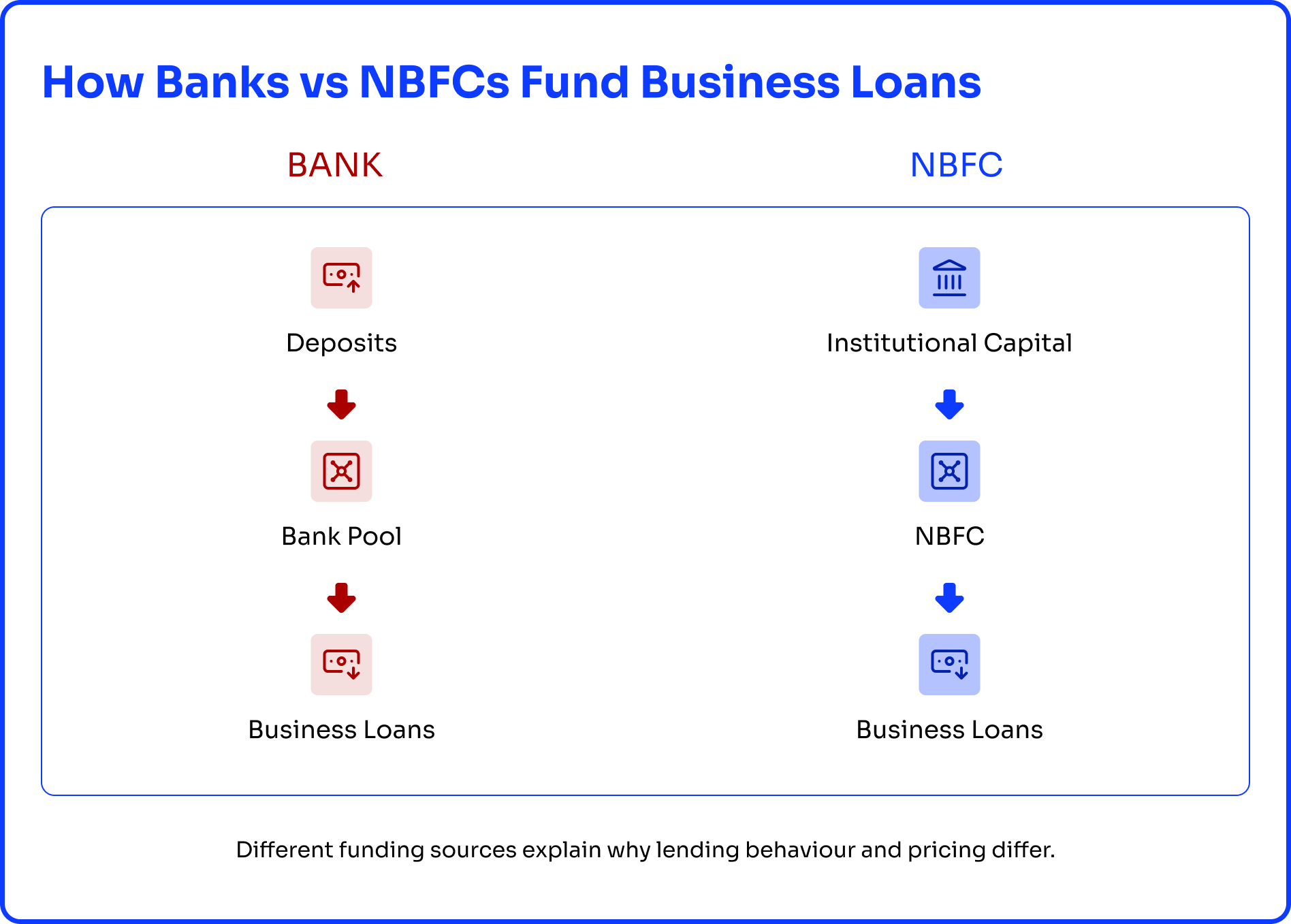

NBFCs operate under a different funding model. They do not rely on public deposits. Instead, they raise capital from banks, institutional investors, and financial markets, and then lend this capital to businesses.

Since their cost of capital is higher, NBFC loans generally carry higher interest rates.

However, NBFCs focus on speed and flexibility. Their evaluation process is often faster and relies more on recent financial data rather than traditional collateral.

Many NBFCs assess businesses using indicators such as recent bank transactions, invoice flows, digital financial records, and short-term revenue patterns.

This approach allows them to approve loans quickly, sometimes within a few days. For SMBs and MSMEs that need immediate funding, NBFCs can provide timely access to capital.

Why many businesses use both lenders

Banks and NBFCs do not necessarily compete with each other. In many cases, they address different financial needs within a business.

Banks are often suitable for structured and long-term financing such as working capital limits, overdraft facilities, expansion funding, and long-term business loans.

NBFCs are often useful for short term financial needs such as covering temporary liquidity gaps, financing invoices, purchasing equipment, or obtaining quick working capital.

Many growing businesses use both lenders strategically. They rely on banks for stable and lower cost credit, while they turn to NBFCs when speed and flexibility become important.

This approach allows businesses to manage both cost efficiency and operational agility.

The role of financial visibility

Whether a business approaches a bank or an NBFC, one factor strongly influences lending decisions. That factor is financial visibility.

Lenders want a clear understanding of how money moves through the business. They look for stable receivables, consistent payment discipline, and predictable cash flow patterns.

Businesses that maintain organised financial records and transparent banking activity often experience smoother lending processes and stronger relationships with lenders.

For this reason, many growing SMBs and MSMEs use financial platforms like Yobo that help them monitor cash flow and manage banking data across multiple accounts. These tools allow founders to track balances, review transaction patterns, and maintain clear financial records when lenders request information.

Final thoughts for founders

Founders can make more informed financing decisions when they clearly understand the difference between banks and NBFCs.

Banks usually provide structured credit at lower interest rates, though their approval processes take time. NBFCs provide faster access to capital but often at a higher cost.

Successful businesses often use both sources of funding depending on their needs. At the same time, maintaining clear financial records, stable cash flow, and organised banking activity helps businesses build stronger relationships with lenders.

In business finance, access to capital often depends not only on opportunity but also on how clearly a business can demonstrate its financial strength.