Most business owners don’t lose money because they’re careless. They lose it quietly through small, everyday inefficiencies that rarely feel urgent but steadily eat into profits.

Here are ten of the most common money leaks and what you can realistically do to plug them.

1. Idle Cash Earning Almost Nothing

Many SMBs and MSMEs keep ₹6–10 lakhs sitting idle across savings or current accounts. This cash usually earns 3–3.5% interest, translating to roughly ₹25K–₹30K annually on ₹8–9 lakhs.

That same money, when moved to liquid mutual funds or sweep-in accounts, has historically earned closer to 6–7% (subject to market conditions), increasing annual returns to ₹55K–₹60K.

The fix starts with visibility. Identify cash that hasn’t moved for more than a week and isn’t earmarked for immediate expenses. Keep 2–3 weeks of operating expenses in regular accounts and move surplus funds into liquid instruments. Once set up, this requires little ongoing effort but pays back every year.

2. Late Payment Penalties That Add Up

Late fees usually don’t look serious in isolation. A missed rent payment here, a delayed utility bill there each costing ₹2,000–₹2,500 in penalty.

When this happens 8–10 times a year, which is common in growing businesses, the total quietly reaches ₹20K–₹25K annually. Most cases are caused by forgotten due dates, approvals getting stuck, or cash sitting in a different account than the one used for payment.

The fix is mostly about making payments predictable instead of reactive. Start by centralizing all recurring bills and vendor payments into a single payment workflow so due dates aren’t scattered across emails and calendars. Schedule payments a few days in advance to create a buffer for approvals or bank delays and ensure the operating account used for auto-debits always maintains a minimum balance. Many businesses also choose secure finance platforms that, with explicit consent, automate bill payments, track upcoming obligations, and proactively alert you when balances may be insufficient removing the need to rely on memory and manual follow-ups.

3. Paying Extra by Using the Wrong Payment Mode

Many businesses default to faster payment modes without considering cost.

Common patterns include:

- Using IMPS for routine transfers (₹5–₹20 per transaction)

- Using RTGS for relatively small amounts (₹25–₹50 per transaction)

- When NEFT, often free or ₹2–₹5, would work just as well

- Ignoring UPI, which is usually the cheapest option and now widely accepted for payments up to ₹1 lakh

Over a year, this habit can lead to ₹15K–₹30K in excess transaction fees.

The most effective way to control transaction costs is to standardize payment routing instead of leaving it to individual judgment. Define clear payment defaults at the business level so teams don’t decide the payment mode ad hoc. Use UPI as the default for low-value vendor payments, where speed and cost efficiency matter most. For larger but non-urgent transfers, standardize on NEFT, which is reliable and typically the lowest-cost option. Restrict IMPS and RTGS to cases where urgency or transaction size genuinely requires it.

As payment volumes grow, this decision-making should be system-driven rather than manual. Many finance teams adopt platforms that automatically route transactions through the most cost-efficient payment mode based on amount, urgency, and bank rules. This creates consistent cost control across teams, improves treasury efficiency, and ensures transaction fees don’t scale unnecessarily as the business grows.

4. Overdraft Charges While Another Account Has Surplus

This issue shows up when businesses operate multiple accounts without a consolidated view.

One account slip ₹50K into overdraft, attracting interest at around 18% annually, while another account holds ₹2–3 lakhs idle. Even short overdraft periods can cost ₹700–₹1,000 per month, adding up to ₹3K–₹5K annually.

Daily balance visibility across accounts, low-balance alerts, and maintaining buffers in auto-debit accounts prevents this almost entirely.

5. Duplicate Payments That Lock Up Cash

Duplicate payments rarely look like losses, but they block working capital.

To escape this, you can use Centralized Payment tracking, basic approval workflows (or switch to automated approval workflows), and duplicate detection before execution drastically reduce this risk.

6. Currency Conversion Losses on International Payments

For SMBs and MSMEs that make international payments, currency conversion is one of the most invisible money leaks.

Traditional banks often apply effective forex margins of 3–5% over the base exchange rate, along with wire transfer fees of ₹1,000–₹3,000 per transaction. On annual international payments of ₹8–12 lakhs, this quietly adds up to ₹30K–₹50K lost every year.

The solution is to be intentional about how international payments are routed. Instead of defaulting to bank wires, many businesses now use specialized forex platforms such as Wise, BookMyForex, Nimo Forex or other RBI-authorized forex providers. These platforms typically offer tighter spreads (often around 0.5–1%), clearer pricing, and lower transfer fees compared to traditional banks.

7. Paying to Maintain Unnecessary Bank Accounts

Over time, many SMBs and MSMEs accumulate bank accounts that no longer serve a clear purpose.

With maintenance fees of ₹400–₹600 per account per month, keeping just two unnecessary accounts costs ₹10K–₹15K annually, excluding the time spent managing them.

An annual account audit helps here. Identify which accounts are actively used, close redundant ones, and negotiate fee waivers where balances justify it.

8. Missing Eligible GST Input Tax Credit

GST input tax credit leakage usually isn’t intentional. It comes from delayed reconciliation, missing invoices, or incorrect categorization.

Businesses eligible for ₹1.5–2 lakhs in ITC often miss ₹30K–₹60K annually due to process gaps. Monthly reconciliation, better expense tagging, and capturing vendor GST details at payment time significantly reduce this loss.

9. Excess TDS Locking Up Cash

In many cases, ₹50K–₹1 lakh gets deducted as excess TDS and remains locked for 9–12 months until refunds arrive.

Even at a conservative 6–7% opportunity cost, this results in ₹5K–₹10K annually in lost value. Better advance planning, collecting certificates where applicable, and filing refunds promptly help reduce this drag on working capital.

10. Time Cost Is Still a Real Cost

Many founders spend 10–15 hours each month on routine banking tasks checking balances of multiple bank accounts, processing payments, reconciling transactions.

Even valuing founder time conservatively, this translates to ₹2–3 lakhs annually. Automating these workflows doesn’t just save time; it redirects energy toward growth and decision-making.

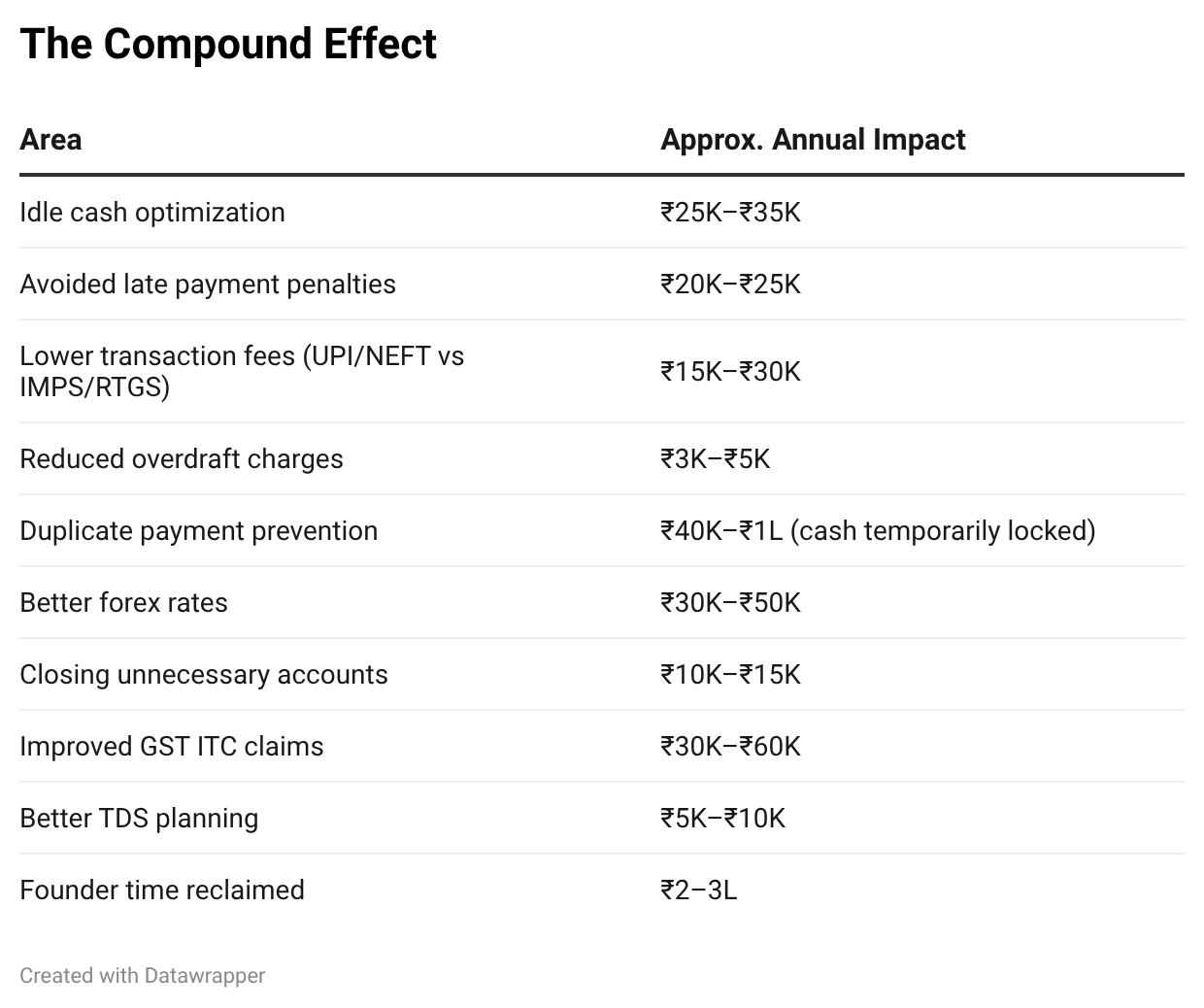

The Compound Effect

Individually, these leaks feel manageable. Together, they quietly drain serious cash.

Note: - if we include the cash that bleeds from Duplication of payments (point 5) which happens rarely the total annual cash impact will be more than 4–5L

Your Action Plan

Start with financial visibility. This week, audit all your business bank accounts to identify idle cash, set up a simple payment calendar with automated reminders, and review recent transaction fees to uncover unnecessary IMPS or RTGS costs impacting your cash flow.

Over the next month, move into cost optimization. Shift surplus funds into higher-yield instruments, tighten vendor payment workflows to prevent duplicate payments, default to cost-efficient payment modes like UPI and NEFT, and close redundant bank accounts that add operational overhead without value.

Within the quarter, focus on scaling efficiently. Automate routine finance operations, establish reliable GST input credit tracking, review TDS planning with your CA to unlock trapped working capital, and reinvest the savings into growth initiatives that directly improve revenue or profitability.

The Bottom Line

You’re not leaving money on the table because you’re bad at business. You’re leaving it because you’re busy running one.

The good news is that most of these leaks don’t require dramatic changes just better visibility, smarter defaults, and a bit of automation. Once fixed, they tend to stay fixed.

The real question is simple: are you comfortable letting ₹4–5 lakhs quietly slip away every year, or would you rather keep that money working for your business?

Stop the Leaks

Yobo helps Indian SMBs & MSMEs plug money leaks automatically. Unified banking, smart payments, AI detection of inefficiencies. Start free, see what you’re leaving on the table.