Many Indian SMBs and MSMEs believe they manage cash prudently, yet they struggle with a silent treasury management problem that rarely shows up in standard financial reports. The issue is not lack of profit, nor poor collections, nor excessive spending. The real problem lies in how liquidity is structured. Large sums remain parked across multiple bank accounts without clear segmentation, earning low savings interest while occasional borrowing fills temporary gaps. The business appears stable on the surface, but capital is not positioned efficiently.

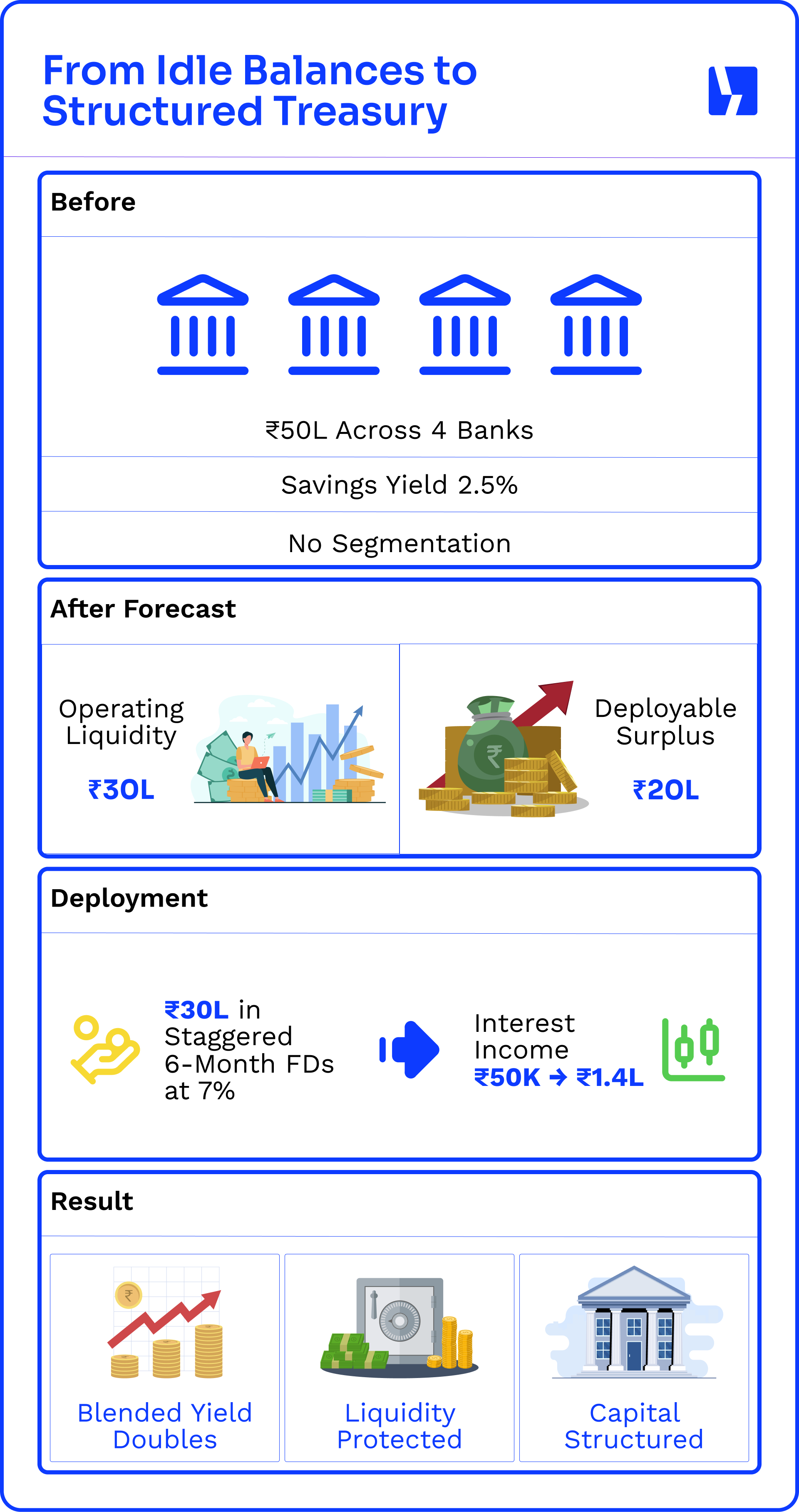

A mid-sized MSME recently faced exactly this situation. The promoters felt reassured because nearly ₹50 lakh sat across four bank accounts at any given time. They called it their emergency reserve. The funds were meant to cover payroll, GST, vendor payments, and unexpected working capital needs. Seeing these balances daily created a sense of security.

However, once the company introduced a structured 90-day cash flow forecast, clarity replaced comfort. By carefully mapping receivable timelines, supplier commitments, statutory outflows, and EMI schedules, the finance team realized that the true operating liquidity requirement rarely exceeded ₹30 lakh. Even during projected low points in the quarter, the business did not require more than that amount to function smoothly. Nearly ₹20 lakh had been sitting idle for months.

The Hidden Cost of Idle Cash

Those balances were earning approximately 2.5 percent per annum in savings accounts. On ₹20 lakh, that translates to about ₹50,000 per year. The number did not look alarming until it was compared with a six-month fixed deposit offering 7 percent per annum. At 7 percent, ₹20 lakh generates ₹1.4 lakh annually.

The additional ₹90,000 per year represents a 180 percent increase in return on the same capital, without increasing risk and without locking funds beyond realistic liquidity cycles. Over five years, assuming similar rates, this difference could exceed ₹4.5 lakh. The business was not losing money due to poor operations. It was losing income due to unstructured treasury management.

From Survival to Predictability

Most MSMEs start in survival mode. The focus is immediate and practical:

Will salaries clear this month?

Can we pay suppliers on time?

When will receivables come in?

As the business stabilizes, cash flow becomes more predictable. Instead of worrying about daily balances, management starts asking: when will we hit the lowest liquidity point this quarter? That predictability reduces stress and brings a sense of control.

You can read more about this stage of cash flow forecasting & management here.

Misaligned Capital and Blended Returns

A closer look often reveals the same pattern. Cash sits idle for long periods. Fixed deposits are opened randomly when surplus feels “visible.” Borrowings at 9% run alongside balances earning 3%. There’s no liquidity structure every rupee is treated the same, no matter when it’s needed.

Take a business holding ₹1 crore across accounts at an average 3% savings rate. That earns ₹3 lakh a year. With better forecasting, it realizes ₹60 lakh is enough for operations, while ₹40 lakh stays unused for at least 90 days.

If that ₹40 lakh is placed in staggered fixed deposits at 7.5%, it generates ₹3 lakh on its own. Total interest income rises from ₹3 lakh to ₹6 lakh. The blended return moves from 3% to about 6%. The capital stays safe but works twice as hard.

This isn’t about taking risk. It’s about fixing structural inefficiency.

Yobo. doesn't only help you identify funds lying around idle but also provides you options on how to choose the best yield for your business.

A Practical Treasury Framework

Mature businesses think of liquidity in layers.

Operating liquidity covers payroll, statutory dues, key vendors, and loan instalments. This money must stay fully accessible.

Tactical surplus is the stable excess beyond that buffer. It can move into short-term deposits aligned with 30–90-day cash cycles.

Strategic capital is meant for expansion, capex, acquisitions, or debt optimization.

Once liquidity is clearly segmented, behavior shifts. Not every balance is treated like an emergency fund. Management can confidently identify deployable surplus. Deposits become planned and structured not random.

Technology and Liquidity Intelligence

Earlier, such discipline required heavy spreadsheet modelling and manual reconciliation. Today, treasury tools can consolidate multi-bank visibility, analyze inflow and outflow patterns, identify stable idle surplus, and suggest deposit tenures aligned with forecast cycles. The purpose is not wealth creation. It is liquidity intelligence.

The Real Shift Is Mindset

Treasury management is not a luxury reserved for large corporates. It is financial positioning for businesses to grow. Saving protects capital, but treasury discipline optimizes it. The difference between earning 3 percent and earning 7 percent may seem small, yet across substantial balances and over several years, that difference compounds into strategic flexibility.

Profitability builds the business. Treasury discipline builds resilience.