Key Takeaways

- SMBs & MSMEs already practice maker-checker informally the real opportunity is to formalize and automate it

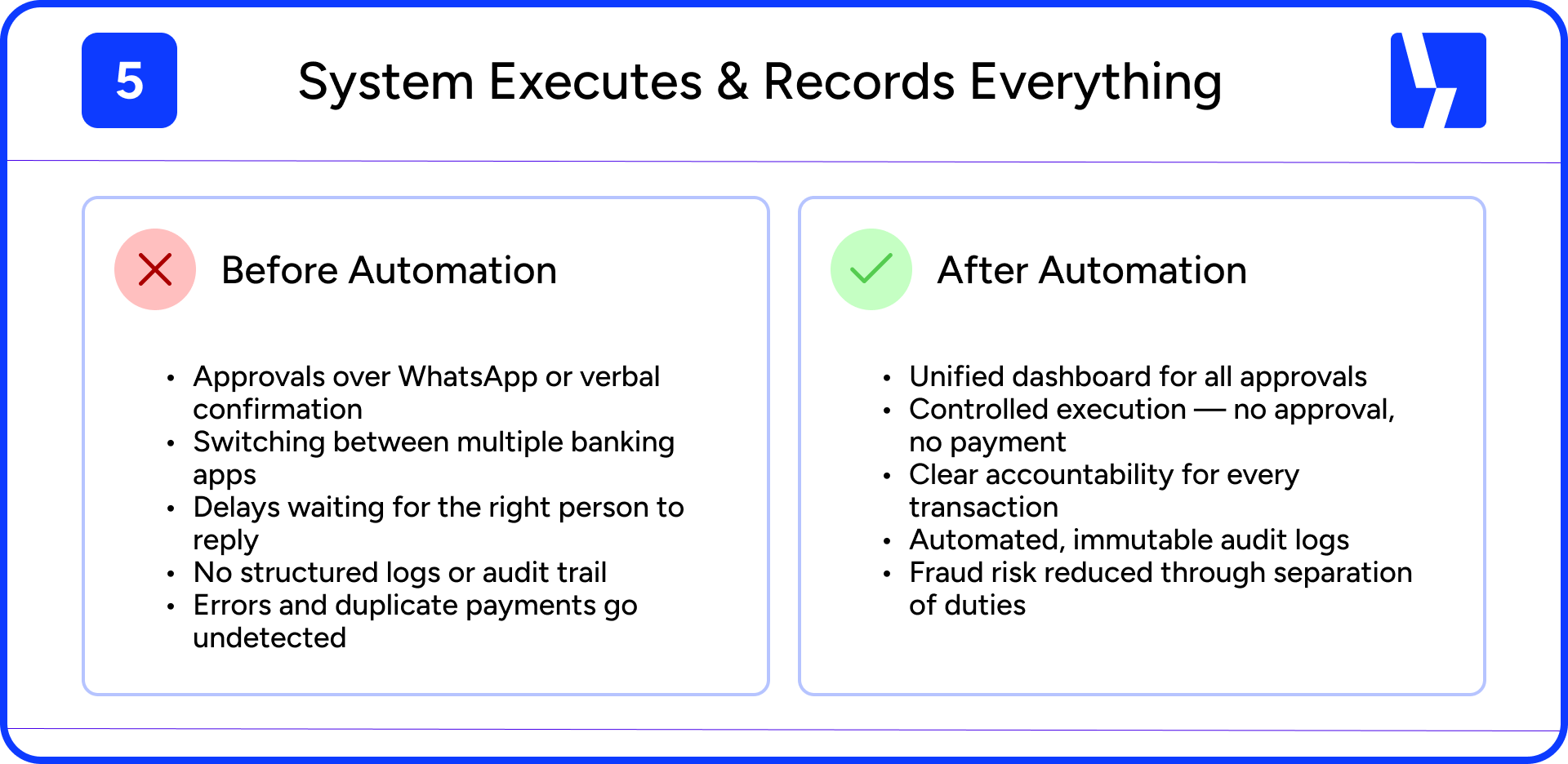

- WhatsApp and email-based approvals create bottlenecks and increase error risk as volumes grow

- Centralized platforms enable structured dual authorization without slowing operations or consuming founder bandwidth

You’re Already using Maker-Checker process Just Not Systematically.

Let's understand with an example

Company X is a growing distribution business. A few years ago, payment approvals were simple. With 30–40 transactions a month, every invoice passed through the founders review before funds were released.

Today, the business processes nearly 200 payments monthly vendor settlements, payroll, statutory dues, advances. Documentation is no longer centralized. Invoices arrive by email. Payment details are shared over WhatsApp. Supporting files sit across systems.

Approvals now happen between meetings.

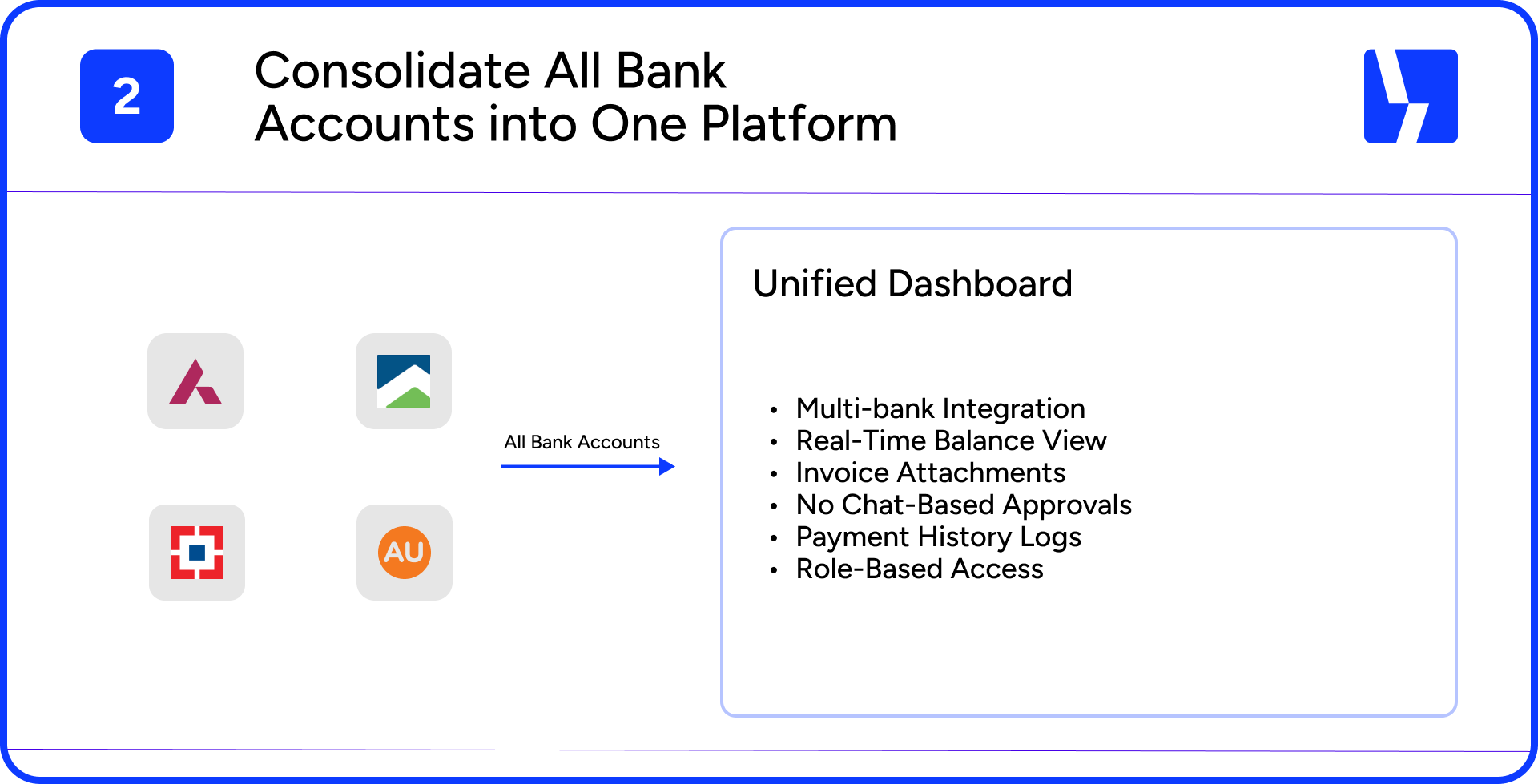

The founder reviews amount quickly, assumes verification has been done, and authorizes release. Liquidity sits across multiple bank accounts, but approvals are granted without consolidated visibility of cash position or upcoming obligations.

One month, a ₹25,000 settlement is processed as ₹2,50,000 due to a single data-entry error. Another time, a duplicate invoice is paid because it was reissued under a new reference. This was the result of fragmented information.

The maker–checker principle still existed one initiated; another approved. At lower volumes, this worked. As transaction velocity scaled, it introduced operational risk.

What Could Have Been Done Differently

Looking back, Company X did not need more oversight. They needed structural financial discipline embedded into their entire process.

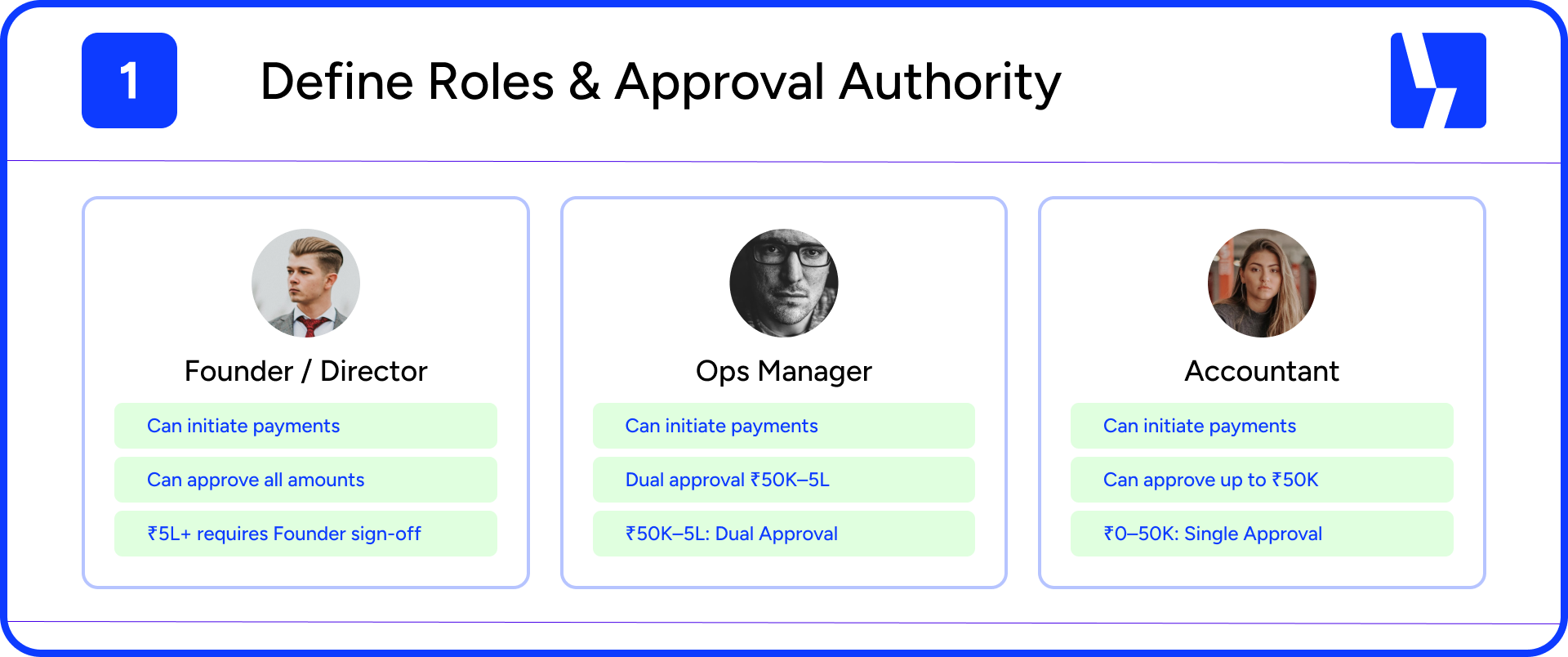

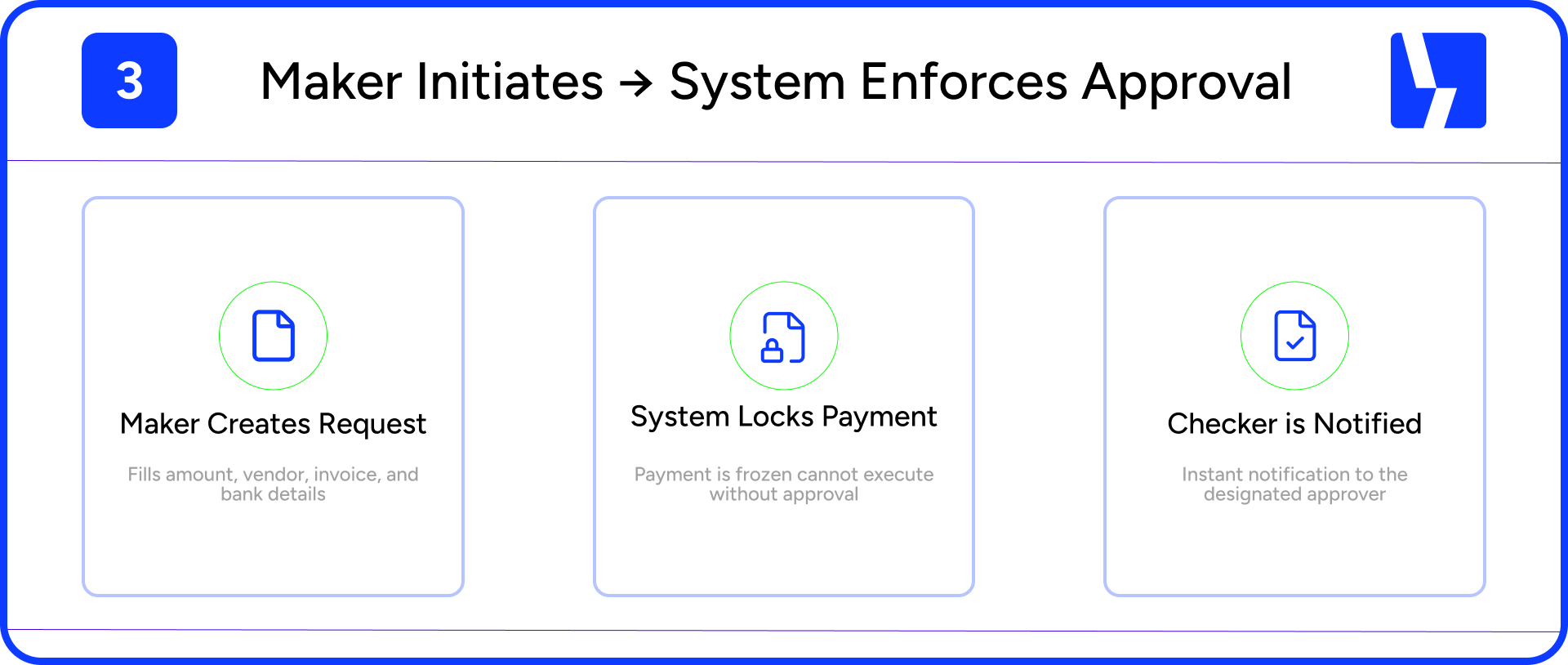

The first step could have been centralizing the entire authorization workflow; they could have moved the maker–checker process into a single controlled environment exactly what Yobo.money provides.

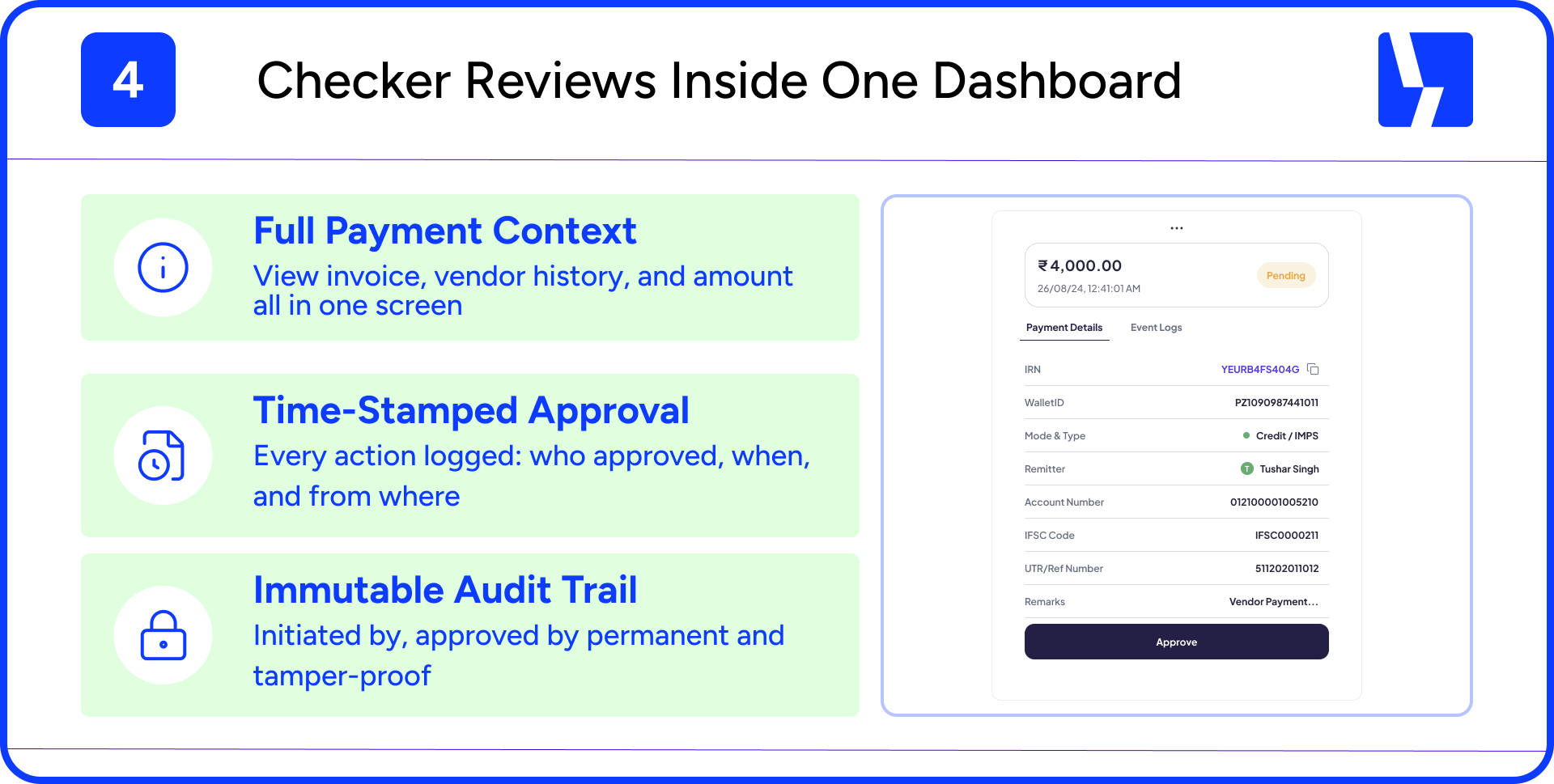

In such a structure, when the accountant initiates a payment, the invoice would be attached at the source. Vendor bank details would be standardized and validated. A transaction cannot not move forward without complete documentation.

More importantly, liquidity visibility would be available at the point of approval. To understand on how to bring back visibility into all your accounts click here

Before authorizing a ₹2,50,000 vendor payout, Company X could have reviewed:

- Consolidated balances across all business accounts

- Scheduled payroll and statutory obligations

- Upcoming fixed outflows

- Available operating buffer

The maker–checker principle remains unchanged, but enforcement becomes system-driven rather than dependent on chats or recollection. Approvals require designated authorization within a structured workflow, with clear role definition and recorded validation. As transaction volumes increase, the process remains stable instead of becoming strained.

How to systematically Implement Maker-Checker

What should you consider

If you see parts of your own business in Company X, don’t ignore it.

You don’t need new principles. You need structure around the ones you already follow.

Centralize your approvals. Define clear roles. Make sure no payment moves without documentation and context. Build visibility across your bank accounts before you authorize funds.

Formalize your controls while volumes are still manageable not after scale introduces avoidable risk.

FAQs

1. Will a structured treasury or payment platform actually reduce my time?

Yes. This reduces back-and-forth communication and minimizes time spent reconciling scattered information.

2. Are these platforms secure for handling business payments?

Reputable platforms are built with bank-grade encryption, role-based access controls, and structured audit trails. With Account Aggregator in play. To understand more on AA Read

3. We’re still a small business. Do we really need this?

If you’re making regular vendor payments, handling payroll, and delegating approvals then yes, structure helps. It’s less about company size and more about how many moving parts you’re managing.

4. Will this make things more complicated for my team?

Not if it’s done properly. In most cases, it actually removes confusion. Instead of approvals sitting in chats or emails, there’s a defined flow. That usually makes things clearer, not heavier.

5. How do we introduce this without disrupting daily operations?

Start by centralizing visibility and formalizing approval roles. Once the workflow is defined, a structured platform can embed those controls into your daily payment process without requiring major operational changes.