If you are running a growing business in India, multiple bank accounts are almost inevitable. You may have started with an HDFC current account. Later added ICICI for better online tools. Opened Axis for a specific client or project. Perhaps SBI still exists because closing it never made it to the priority list. Before you know it, your morning begins not with customers or strategy, but with three banking apps, a notebook, and mental arithmetic.

This is not poor planning. It is the natural outcome of how Indian businesses grow. In fact, internal research across Indian SMBs & MSMEs shows that most operate with close to three active bank accounts. Each decision made sense at the time. Together, they quietly create operational friction. The problem is not multiple bank accounts. The problem is managing them without a system.

Let us talk about how to do this properly.

Why Businesses End Up with Multiple Bank Accounts

Most SMBs & MSMEs do not wake up one day and decide to complicate their lives. Multiple accounts usually emerge for practical reasons. Different banks excel at different services.

One offers better transaction pricing. Other processes loans faster. A third has superior branch support in a specific city. Bank relationships matter. Your working capital loan may sit with HDFC, while collections flow better through ICICI. Some clients insist on dedicated project accounts, especially in manufacturing, exports, or services with escrow-like structures. Geography plays a role. An SBI branch in Chennai may be operationally stronger than a private bank, while Mumbai tells a different story. Payment gateways often work more reliably with specific banks. And finally, risk diversification. Many founders do not want all their liquidity tied to a single institution.

All of this is rational. The issue begins when visibility does not scale with complexity.

The Hidden Cost of Multi Bank Chaos

The real cost of managing multiple bank accounts is rarely visible on a P&L. But it is very real.

Time Cost

A typical routine looks like this. Checking balances across three banks every morning. About 15 minutes. Downloading statements from each bank at month end. Three to four hours. Answering basic questions like which account a vendor was paid from. Ten minutes at a time. Over a month, this quietly adds up to nearly 15 hours of founder or senior management time. At even a conservative valuation of ₹2000 per hour, that is ₹30,000 a month spent on administrative visibility, not decision making.

Money Cost

Missed early payment discounts because funds were available, just not in the right account. Overdraft or penalty charges when one account dipped negative while another had surplus cash. Idle balances earning basic savings interest while higher yield options existed. Late compliance payments because funds were parked elsewhere. These are not accounting errors. They are visibility failures.

Opportunity Cost

Time spent reconciling is time not spent on customers. Mental energy spent tracking money is energy not spent on strategy. Decisions get delayed because clarity takes effort.

Compliance and Risk Cost

Fragmented audit trails. Difficulty tracking approvals and payment sources. Stress during audits because data lives in too many places. None of these scales well.

Seven Practical Ways to Manage Multiple Bank Accounts Well

1. Consolidate Where It No Longer Serves You

Start with an honest audit. What is the purpose of each account today, not two years ago. Which accounts duplicate functionality. Which ones exist only because closing them feels inconvenient.

Most SMBs & MSMEs can operate efficiently with two to three well defined accounts. Anything beyond that should have a clear reason. One customer reduced five accounts to three and cut reconciliation time by more than half.

Fewer accounts do not mean less control. They usually mean more.

2. Assign Clear Roles to Every Account

If multiple accounts are necessary, give each one a job. One account for daily operations, salaries, utilities, routine vendor payments. One account for client receipts and project related inflows. One account for reserves, taxes, and buffers. When roles are clear, confusion disappears. You always know where to look and where to act.

3. Stop Logging into Multiple Banking Apps

This is where modern infrastructure changes the game.

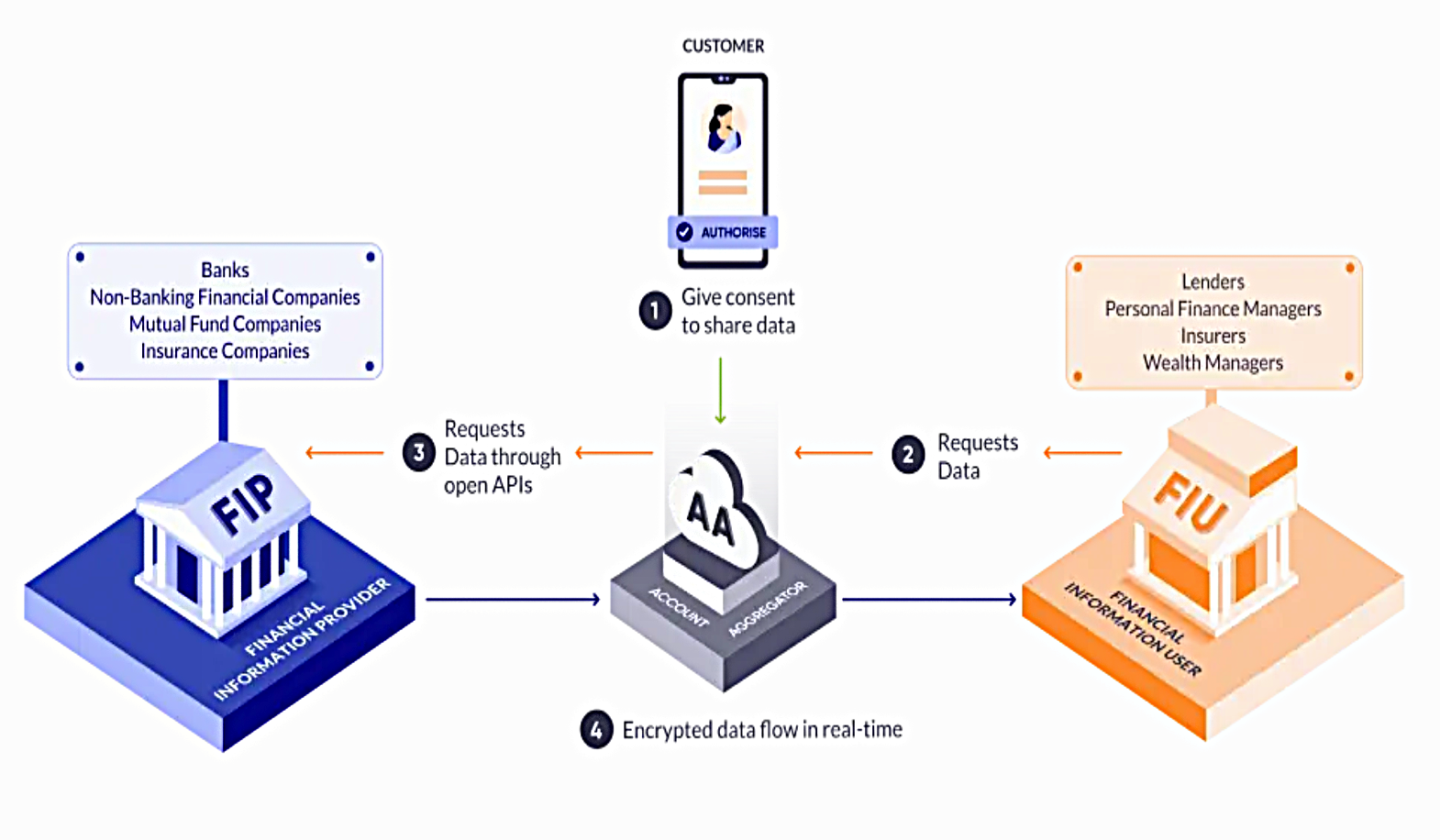

India’s Account Aggregator framework allows businesses to view multiple bank accounts through a single, secure dashboard. Instead of checking three apps, you see one consolidated view. Total cash position across all banks. Unified transaction feed. Account level detail when required. Near real time updates. What used to take fifteen minutes now takes one.Over a month, this alone saves nearly a full working day.

4. Automate Reconciliation Properly

Manual reconciliation is not a rite of passage. It is an inefficiency.

Modern tools automatically fetch statements, categories transactions, and prepare clean exports for accountants. Once trained on your business patterns, categorization accuracy is extremely high. What earlier took hours can now be done in minutes.

Your CA gets cleaner data. You get your time back.

5. Use Alerts Instead of Constant Monitoring

Control does not come from checking more often. It comes from knowing when something needs attention.

Set alerts for low balances, large payments, unusual transaction patterns, idle cash, and failed or recurring payments. Banks offer some of this. External tools offer consolidated alerts across all accounts.

Either way, let the system notify you. Do not babysit it.

6. Standardize the Process

Good financial hygiene is boring by design. Define simple routines. A weekly balance check. A fixed day for vendor payments. A monthly export for accounting. When the process is predictable, it stops draining mental energy.

7. Optimize Cash, Do Not Just Track It

Visibility enables optimization.

Once you see all your money in one place, patterns emerge. Cash sitting idle for weeks. Accounts carrying more buffer than required. Opportunities to move surplus into liquid funds, sweep facilities, or short-term instruments.

Most SMBs & MSMEs discover ₹2 to ₹3 lakh of idle cash once visibility improves. At even a modest yield difference, that translates into meaningful monthly gains.

Why Account Aggregator Matters

For businesses, this means security, compliance, and convenience without compromise. It is how modern multi bank management should work.

A Real-World Example

Rajesh runs a 25-person manufacturing unit in Pune. He operated four accounts across HDFC, ICICI, Axis, and SBI. Every morning involved switching apps, noting balances, and calculating totals. With a unified dashboard, his daily visibility dropped to under a minute. More importantly, the system flagged ₹2 lakh sitting idle in an old SBI account. That money was moved into a higher yield option. The gain was modest in isolation, but it came from money he had forgotten existed.

That is the power of visibility.

A Simple Action Plan

This week

List all active accounts. Write down their purpose. Identify redundancy.

Next week

Adopt a multi-bank dashboard using Account Aggregator. Set up basic alerts.

This month

Review consolidated data. Identify idle cash. Optimize allocation. Quantify time saved.

The Bottom Line

Multiple bank accounts are not a problem. Managing them with outdated methods is. With the right structure and modern tools, multi-bank management becomes quiet, efficient, and almost invisible.

The real question is not whether you should simplify. It is whether your time is worth more than administrative friction.